AI in Accounting: 7 Use Cases And Benefits

Accounting has automated repetitive work for decades, from spreadsheet macros to rules-based scripts that move numbers between systems. What changed recently is the kind of work that automation can reach. Modern AI does not just copy a value from an invoice into a ledger field; it reads the invoice, decides which account the charge belongs to, drafts the variance commentary a controller would have written by hand, and flags the transaction that does not fit the pattern of the thousand before it. The accountant’s role moves up the stack, from recording and reconciling toward reviewing, explaining, and advising.

That shift comes with a condition: an AI system in accounting is only as good as the financial data it can reach and the accuracy the profession is required to hold. A model that drafts confident commentary from incomplete numbers is worse than no model at all, because the error carries an auditor’s expectation of correctness. This post explains what AI in accounting means, why the field is adopting it now, how it works, the benefits it delivers, and seven use cases already in production.

What is AI in accounting?

AI in accounting is the application of machine learning, natural language processing, and generative models to the tasks accountants perform: capturing and classifying transactions, reconciling accounts, preparing financial reports, supporting audits, detecting fraud, and forecasting. It sits on top of an older layer of automation (rules-based scripting and robotic process automation, or RPA) and extends it from fixed, predictable steps to judgment-shaped work that previously required a person.

The distinction matters because the two are often conflated. Rules-based automation follows instructions written in advance: if the vendor is X, code the expense to account Y. It is fast and exact, but it breaks the moment an input does not match a rule, and someone has to anticipate every case. AI learns the mapping from examples instead, so it generalizes to invoices, transactions, and documents it has not seen in that exact form. The trade-off is that it is probabilistic: a most-likely answer with a confidence, not a guaranteed-correct one, which is why human review stays in the loop for anything that lands in a filed financial statement.

Most products combine several building blocks: document AI and optical character recognition (OCR) to turn invoices, receipts, and contracts into structured fields; machine-learning classification and anomaly models to code transactions and surface entries that deviate from a learned norm; large language models (LLMs) to generate narrative (report commentary, audit memos, plain-language answers about the numbers) and summarize documents; and RPA and orchestration to carry the output between systems, so a classified transaction posts and a flagged exception reaches a reviewer.

Put together, AI in accounting is less a single product than a layer spanning capture, classification, reporting, and analysis: generative models handle the language, machine learning handles the scoring and prediction.

Why AI is transforming the accounting industry

Several pressures are arriving at the same time, and AI addresses more than one of them, which is why adoption has moved from pilot to budget line in many finance functions.

The talent pipeline is shrinking while the work is not. U.S. colleges awarded 6.6% fewer accounting degrees in the 2023–2024 academic year than the year before (the AICPA’s 2025 Trends report), even as transaction volumes and reporting requirements grow and the Bureau of Labor Statistics projects more than 120,000 openings for accountants and auditors a year. AI does not replace the judgment of an experienced accountant, but it absorbs the high-volume, low-judgment work (data entry, matching, first-pass reconciliation) that junior staff used to carry, which lets a smaller team cover the same ground.

The close cycle keeps getting shorter. Stakeholders expect faster reporting, and in some cases something closer to continuous visibility than a monthly close, yet half of finance teams still take longer than five business days to close and only 18% close in three or fewer (Ledge 2025 month-end close survey). Manual reconciliation and consolidation are the bottleneck, and they are exactly the steps AI can compress.

Regulatory and audit complexity is rising. More disclosure requirements, more jurisdictions, and more scrutiny mean more evidence to gather and more to test. AI lets a team test full transaction populations rather than samples, and keep controls running continuously rather than checking them after the fact.

The role itself is moving toward advisory. As recording and reconciling become automated, the value a finance team adds shifts toward interpretation, planning, and counsel, and AI accelerates that shift by handling the mechanical layer. The market reflects it: Grand View Research estimated the AI-in-accounting market at roughly $4.9 billion in 2024 and projected a compound annual growth rate near 40% through 2033, and while firms’ estimates of the absolute size vary widely, they agree on the steep slope.

These pressures reinforce each other: a thinner talent pool makes automating routine work urgent, faster reporting cycles make manual steps the constraint, rising compliance load makes full-population testing attractive, and the advisory shift gives accountants somewhere more valuable to spend the time AI returns. None is decisive alone, but together they explain why the adoption curve has steepened rather than flattened.

How AI works in modern accounting processes

Inside a real finance function, AI rarely shows up as one model. It shows up as a chain: capture, classify, reconcile, report, and review, with a different technique doing each job and data moving between them.

Capture and reconcile. Document AI sits at capture: an OCR-plus-LLM pipeline extracts the vendor, amount, line items, tax, and dates from an invoice (or receipt, or contract) into structured fields, regardless of how each vendor formats it. Machine learning then classifies and reconciles, predicting the account, cost center, and tax treatment for each transaction from the company’s own coding history, and matching payments to invoices and bank lines to ledger entries, including the partial and many-to-one matches that defeat simple rules.

Score and write. Anomaly models run over the classified data, learning what normal looks like for a given vendor or account and scoring how far each new entry sits from it, which is how duplicate payments and unusual journal entries surface for review. Generative models do the writing: an LLM drafts variance commentary, summarizes a long audit file, and turns a question like “why did travel expense jump in Q3” into an explanation grounded in the underlying figures.

Across capture, classification, scoring, and writing, the same assumption runs underneath: each step is only as good as the financial data the model can actually reach. That makes the data layer, more than the choice of model, the part of an AI accounting stack that most often decides whether its output can be trusted.

Key benefits of AI in accounting

The pitch for AI in accounting is sometimes flattened to “it saves time.” It does, but the benefits finance leaders actually weigh are more specific, and several are about risk and accuracy rather than speed.

Accuracy and fewer manual errors. Manual data entry and copy-paste reconciliation are a reliable source of mistakes, and the cost of an error is high because it can flow into a filed statement. AI removes most of the keystrokes, and anomaly models catch the errors that slip through, so accuracy improves on two fronts at once.

Speed and a faster close. When capture, classification, and reconciliation run continuously instead of in an end-of-period scramble, the close compresses from weeks toward days and reporting moves closer to real time. The constraint stops being how fast people can process transactions and starts being how fast they can review exceptions.

Cost, capacity, and advisory time. Automating high-volume work lets a finance team handle more transactions without growing headcount, which matters most when the talent pool is tight. The capacity freed is redeployed toward the interpretation, planning, and counsel that the profession is shifting toward, which is both higher-value work and harder to automate.

Continuous controls and audit readiness. AI lets controls run on every transaction rather than on a sample checked after the fact, and it keeps an evidence trail as it goes. The result is a function that is audit-ready continuously rather than one that assembles evidence under deadline.

Fraud and risk detection. Models that learn normal behavior surface the transactions that deviate from it, and graph-based analysis catches the relationship patterns (circular payments, related-party networks, collusion) that per-transaction rules miss. This is detection at a scale and connectedness that manual review cannot match.

Read together, these benefits cluster into two themes: AI raises the accuracy and speed of the mechanical work, and it raises the capacity and reach of the analytical work. Most products start with the first theme because it is easiest to measure. The second, where connected financial data feeds genuinely connected analysis, is where the larger value sits, and it depends on whether the AI can reach a connected view of the underlying financial data.

7 generative AI use cases in accounting

The benefits above are abstract until they attach to specific work. Here are seven places where AI, and generative AI in particular, is already running in production accounting workflows.

1. Automated bookkeeping and transaction categorization

The most widespread use case is also the most mechanical. AI codes incoming transactions to the right accounts, cost centers, and tax treatments by learning from a company’s own history rather than a generic rule set, and reconciles continuously instead of at period end. Generative models layer on top to explain a categorization in plain language and ask a clarifying question when a transaction is genuinely ambiguous, turning reconciliation from a batch chore into a running conversation with a few exceptions.

2. Generative financial reporting and narrative drafting

Producing the numbers is half the reporting job; explaining them is the other half. Generative models draft the narrative layer (management commentary, variance explanations, a board-deck discussion, a first pass at management’s discussion and analysis) directly from the figures, and the accountant moves from writing to reviewing, which is faster and more consistent across periods. The accuracy caveat is real: the draft is only as good as the data the tool can see, and a human signs off before anything is filed.

3. Intelligent invoice and document processing

Accounts payable and receivable run on documents that arrive in every possible format. AI extracts the structured fields from an invoice, receipt, or remittance, performs the three-way match against the purchase order and goods receipt, and routes only genuine exceptions to a person. Generative models extend older OCR by handling layouts they were not trained on and reading unstructured terms (payment conditions, discounts, contract clauses) a fixed template would miss, shrinking the share of documents that need manual touch.

4. Audit automation and sampling

Audit has historically relied on sampling because testing every transaction by hand was impossible; AI removes that constraint. Models test full populations, score every entry for risk, and surface the ones that warrant a closer look, while generative models draft working papers, summarize audit files, and explain why a transaction was flagged. The auditor’s judgment stays central, but it now applies to a risk-ranked full population rather than a random sample, and the documentation drafts itself as the work proceeds.

5. Fraud and anomaly detection

AI detects fraud on two complementary levels. Per-transaction anomaly models learn what normal looks like for each vendor, account, and employee and flag deviations (duplicate payments, round-number invoices just under an approval threshold, off-hours journal entries). Relationship-level analysis goes further, finding patterns that only appear when records are connected: a vendor sharing a bank account with an employee, circular flows between related entities, an approval network that concentrates suspiciously. The first level catches the suspicious transaction; the second catches the suspicious structure, which is usually where organized fraud hides.

6. Cash flow forecasting and financial planning

Forecasting is where machine learning has the clearest edge over a spreadsheet. Driver-based models learn the relationships between business activity and cash, incorporate far more history and variables than a manual model practically can, and run scenarios on demand. A generative interface lets an FP&A analyst ask for a downside scenario or an explanation of a variance in plain language and get back both the numbers and the reasoning. The forecast is still a model of an uncertain future, but a better-informed one, refreshed continuously rather than rebuilt each cycle.

7. Conversational finance copilots

The newest use case is the natural-language interface to the numbers themselves. A finance copilot lets a controller ask “which customers are more than sixty days past due and over their credit limit” or “show me every journal entry that touched the goodwill account this quarter” and get an answer from the actual financial data, without writing a query or building a report. The same pattern powers tax and regulatory research assistants. A copilot’s quality is set almost entirely by the data it can reach and how well it understands that data’s structure, which is why grounding it in a complete, well-modeled view of the financial systems (rather than a single export) separates a useful copilot from a confident but unreliable one.

Grounding AI in connected financial data

Run back through those use cases and one dependency sits underneath all of them: the financial data the AI can actually reach. Every one assumes the model can get to the right numbers, and in most organizations that data is fragmented across the general ledger in one system, sub-ledgers and AP/AR in others, master data on vendors and customers in the ERP, bank feeds from outside, and a meaningful share of the truth still in spreadsheets. An AI tool that can see only one of these answers narrow questions well and connected questions badly.

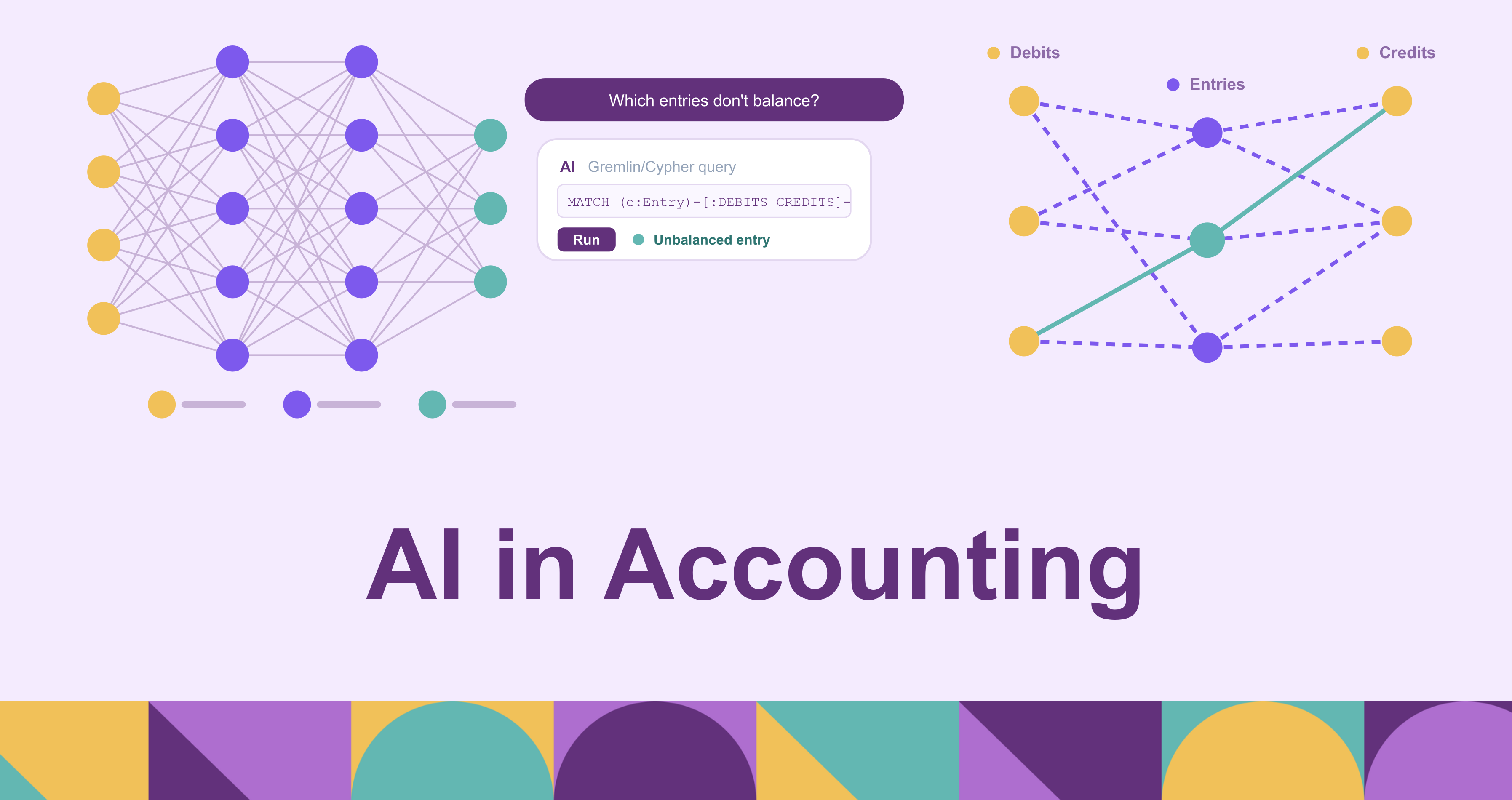

And the questions that carry the most risk in accounting are connected questions, including two of the uses just described. Detecting a fraud ring means following the relationships between a vendor, the employee who approved its invoices, and a shell entity that shares a bank account or address. Tracing a restated figure in an audit means walking backward from a balance through the journal entries and sub-ledger postings that produced it. Consolidation means matching intercompany transactions across legal entities that each keep their own books. These are multi-hop, relationship-shaped problems. Row-by-row queries answer them with brittle chains of joins, and flat document retrieval (the pattern behind many LLM tools) does not answer them at all, because the answer lives in how records connect, not in any single record.

This is where a graph layer earns a place in the stack. Representing financial data as a graph (accounts, vendors, employees, and transactions as nodes, and the relationships between them as edges) lets these connected questions be expressed directly as traversals rather than reconstructed from joins. One way to add that layer without moving the data is an ontology layer between the underlying systems and the AI tool. PuppyGraph takes this approach: it defines a graph schema over existing ERP, ledger, warehouse, and lakehouse tables and queries them in place, with no ETL pipeline copying data into a separate graph database. The tables stay where they are; PuppyGraph is the compute layer that runs graph traversals (in openCypher and Gremlin) across them.

The ontology does two jobs here. As a semantic model, it gives an AI tool a map of what a “vendor,” an “intercompany transaction,” or a “related party” actually is in this organization’s data, so the tool grounds its queries in real entities rather than guessing at table and column names. And because the schema is enforced at query time, a traversal referencing an entity or relationship the ontology does not define is rejected before it runs, and the system returns structured, model-readable feedback explaining the violation in domain terms. That feedback lets the tool correct itself rather than silently return a plausible but wrong answer, which is the accounting version of a hallucination that matters: not a typo, but a number that looks right and is not. A useful consequence is that a tool wired to read data only through this layer can reach only what the ontology exposes, so entities left out of the schema stay out of reach. That is a property of how the deployment is configured rather than a security feature in its own right, and it holds only when the tool has no separate channel to the warehouse. PuppyGraph is used by companies including Coinbase, Dawn Capital, and Prevalent AI, who run graph queries over their existing tables rather than standing up and syncing a second database to do it.

None of this replaces the models that capture, classify, and draft; it gives them a dependable view of the data they reason over. That connected view is what turns the fraud, audit, and consolidation work from pattern-spotting on one table into analysis that follows the relationships where the risk actually lives.

Conclusion

AI has moved accounting past the automation of keystrokes into work that reads, writes, and reasons over financial data: coding transactions, drafting reports, testing full audit populations, detecting fraud, and forecasting cash. The benefits are concrete (accuracy, a faster close, continuous controls, capacity for advisory work) and the use cases are in production rather than on a roadmap. But as the previous section argued, the output is only ever as trustworthy as the connected financial data the AI can reach, and in a profession held to an auditor’s standard of correctness, that data foundation matters as much as the models on top of it.

Try the forever-free PuppyGraph Developer Edition and book a demo with the team to see how openCypher and Gremlin queries run over warehouse and lakehouse tables, with no graph-specific ETL, so an AI accounting tool can trace the relationships across ledger and ERP data that row-by-row and flat retrieval miss.

Sa Wang is a Software Engineer with exceptional mathematical ability and strong coding skills. He holds a Bachelor's degree in Computer Science and a Master's degree in Philosophy from Fudan University, where he specialized in Mathematical Logic.